Executive Summary

An Ecosystem at a Defining Inflection Point

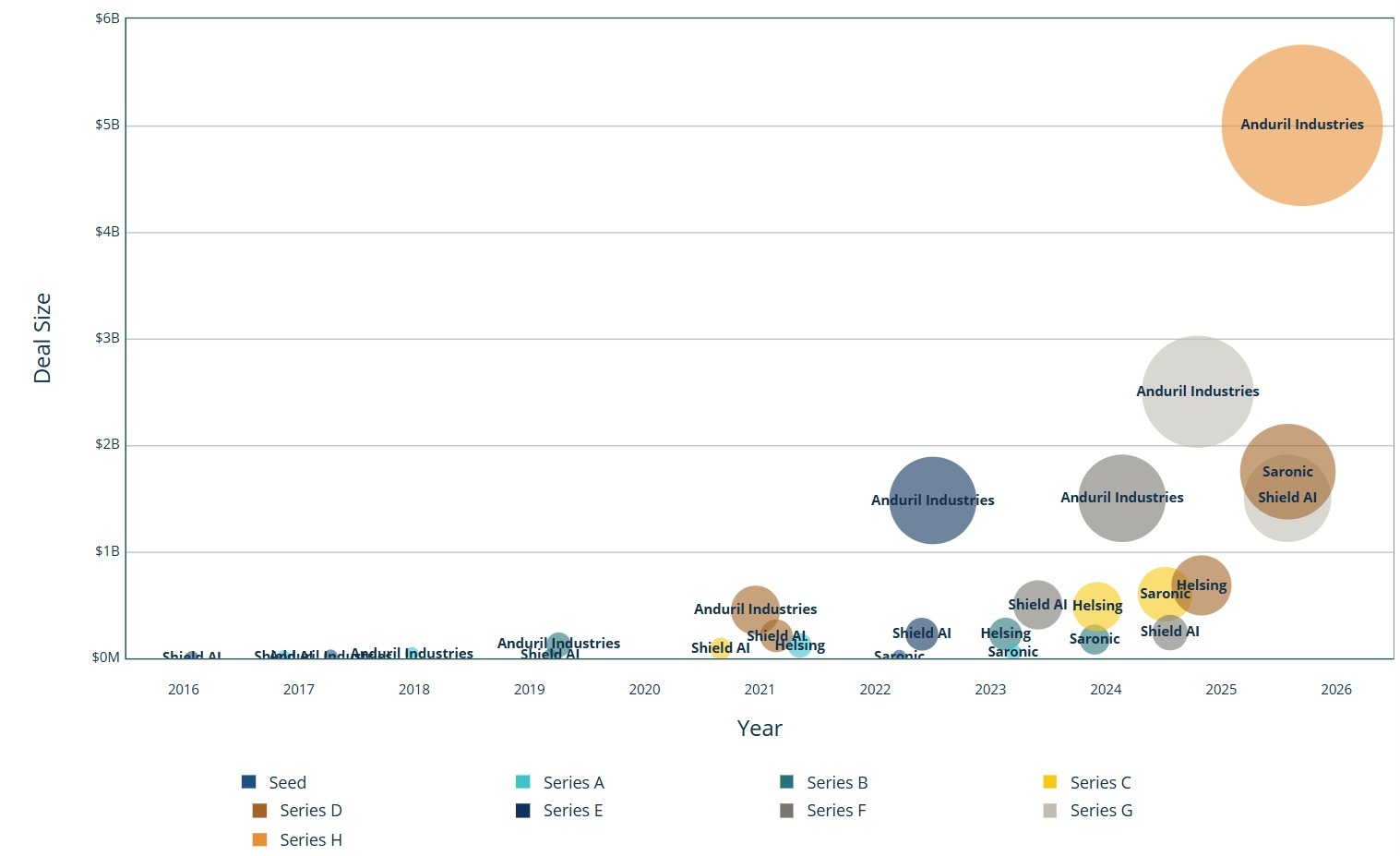

Israel's defense-technology ecosystem stands at a defining inflection point. Since October 7, defense innovation has shifted from a specialized sector to a central pillar of national resilience. Talent mobilized rapidly. Capital reoriented. Government procurement accelerated. Founders with direct battlefield experience began building companies at unprecedented speed.

The question now is no longer whether Israel can innovate under pressure. It is whether Israel can convert urgency into durable industrial capability.

This report examines:

- The size and structure of Israel's defense-tech ecosystem

- Capital and procurement flows

- Early-stage bottlenecks

- The strategic role of pre-seed and early growth capital

- The Core Challenge

- The transition from battlefield validation to institutional delivery

- The path toward global scale, particularly in the United States

Israel has always excelled at improvisation. The challenge ahead is industrialization: transforming battlefield credibility into repeatable product development, scalable manufacturing, procurement fluency, and global export capacity.

As operators working closely with early-stage defense founders, government stakeholders, and capital partners across the ecosystem, we see firsthand where momentum converts into deployment and where it stalls. Our vantage point sits at the intersection of pre-seed architecture, operational validation, and procurement reality. This report is not a theoretical analysis of the sector. It is a synthesis shaped by direct engagement with the founders building, the institutions buying, and the investors underwriting the next generation of Israeli defense capability.

.png)